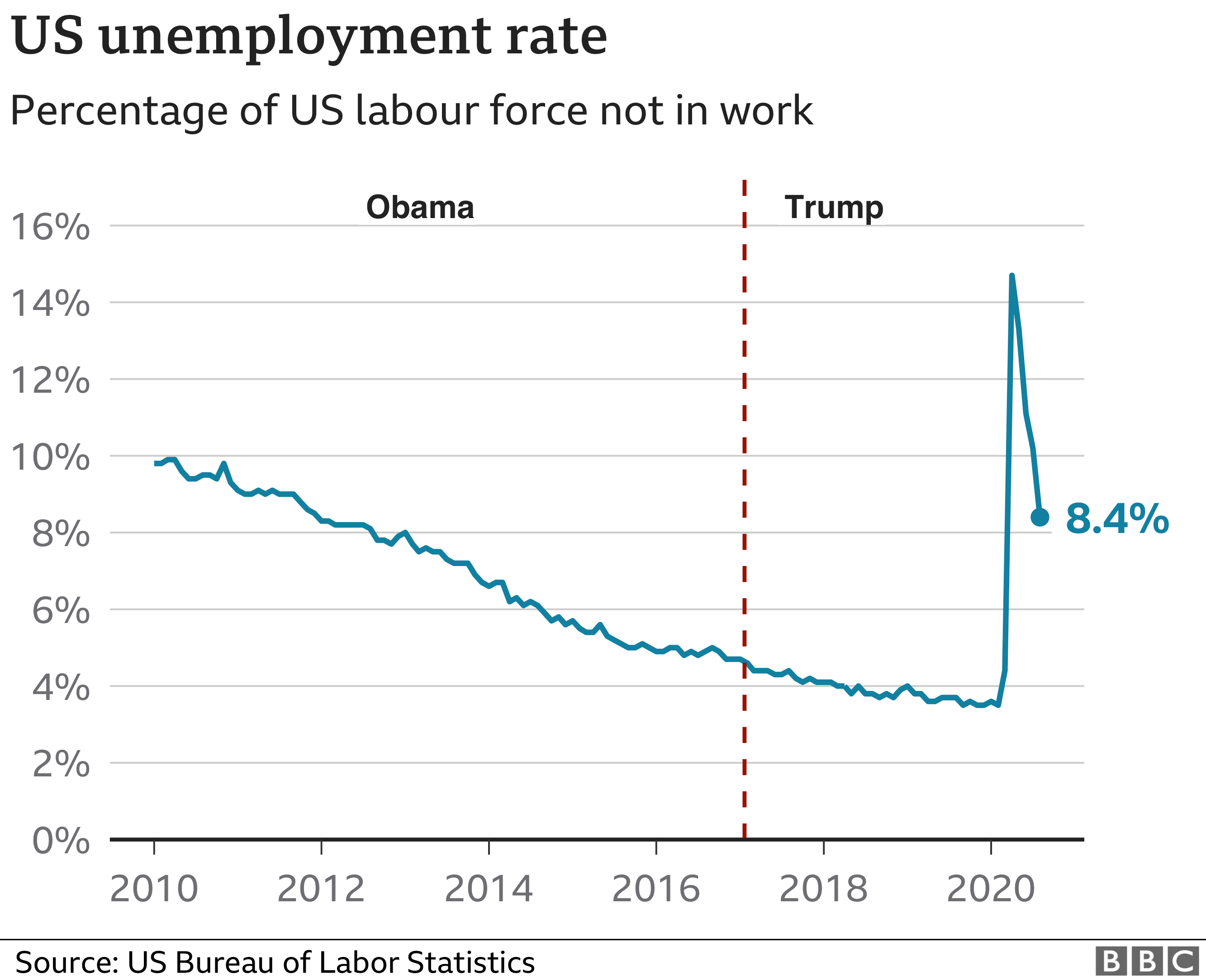

The US Bureau of Labor Statistics reported on Friday that America added 1.37 million jobs in August. It immediately resonated positively, as it marked the fourth straight month of job growth after the economy fell into the pandemic hole and the country experienced historic job losses, and the number slightly exceeded the 1.35 million additions widely expected by the pundits. The media headlines were all over the visible drop in the official unemployment number from 10.2% in July to 8.4%.

To be sure, unemployment has now retraced more than 50% from the blow-out peak at 14.7% in April, but, as always, the devil is in the detail, or should we say in the fine print. For example, the Bureau noted that the headline employment number in August was boosted by staff for the US Census, which hired 238,000 temporary workers during the reference period for the non-farm payroll report. It is to be assumed that most of these will be missing again in September.

Then, those unemployed 27 weeks or longer, or otherwise called long-term unemployed, surged from 9.2% to 12% in August. There is a real worry that an increasing portion of the temporary lay-offs is in the process of becoming permanent. Many of them will no doubt have a harder time finding employment again. It is clearly a sign of continuing underlying weakness in the overall economy and poised to delay any incremental recovery.

Also, the often dismissed labour participation rate doesn’t leave much hope of normalisation. While it has slightly notched up from July, by 0.3% to 61.7% in August, we are way below the average of over 63% pre-pandemic. As noted many times in this space before, the employment situation may not even change much for the better, but the unemployment rate as a ratio can be supported by a declining registered working population.

Markets immediately reacted to the refrain of the upbeat headline numbers, though. 10-year rates rose from 64bp pre-report, to 72bp into the close of the Friday session. But please… it means nothing in the scheme of things. No one is apparently buying Jay Powell’s recent rallying cry for higher inflation, else the long end would have long broken out on the up. And the 2/10-year curve has since his speech a couple of weeks ago defied any steepening, the opposite of what the Fed desires.

Looking through the fundamental rubble, I think it is fair to say that we are a long way from home still. The economy is improving gradually, but what else was there to expect but a mean reversion post that crash into no-man’s land. And to be fair, in the context of the trillions of new money thrown at the system, the recovery is modest at best. The labour market is and will for some time remain dislocated. Don’t be fooled by a few well-sounding headline numbers.

Let’s be real here. Despite an exploding money supply situation, GDP and composite economic indicators are sinking. Despite the unprecedented expansion of the Fed’s balance sheet, eclipsing the 7 trillion mark again last week, the velocity of money has hit rock-bottom and the stimulus is deflagrating as quickly as it is being produced. And along the declining velocity of the M2 money stock budget deficits and national debt explode in tandem. Not a pretty picture overall.

It might take years to get back to where we were if that was even possible. The nature of the economy, and with it our entire societal structure, is likely to change irrevocably. It should not surprise us that the masses are irritated and try to cling on to their previous lives that may forever be lost. Add to this a deeply divided population that is meant to choose from two leadership concepts that could not be more bifurcated and further apart from each other… we are walking on thin ice here.