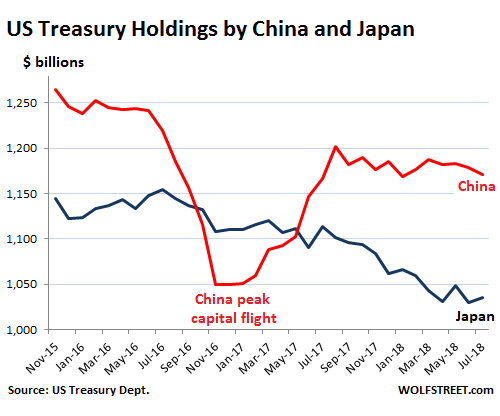

Much ado is being made in the mainstream media of the most recent TIC report capturing foreign US Treasury holdings for October. As per the release, China’s holdings have fallen for five consecutive months and to the lowest level in one and a half years. From September the balance decreased by 12.5 billion dollars to 1.138 trillion. Needless to say that China remains the largest holder of Treasuries, except for the Fed.

Naturally, the press made much more of it than is necessary. Commentaries around China reducing their exposure due to the trade war and the worsening relationship with America have been making the rounds. It so happened that October also accounted for a decrease in China’s total foreign reserves, by 1.1% to 3.05 trillion dollars, and so, the narrative of the economy being in trouble and heading for a crash landing have re-emerged.

Nonsense doesn’t begin to describe it. First of all, the US Treasury only releases the TIC data with a 2-month delay. While this is better than nothing and provides at least a sense of where things are going, October numbers are hardly an up-to-date appraisal of foreign fund flows into the US government market. Too much has happened during the past 2 months, and we will only know in February whether the recent rhetoric, the G20 truce, and the Huawei arrest have had any impact.

Secondly, it is understandable for the media to jump at every number related to China that is moving south, as even the US president has made this a competition about what economy or what stock market is performing better these days, but the change in Treasury holdings of a mere 1% is a rounding error at best. It was rather rooted in a routine portfolio rebalancing than anything else and doesn’t really make any difference to the whole.

So, no, the PBoC will not throw kitchen sink out and trash the Treasury market because the Chinese leadership happens to be disgruntled. And just to keep things in perspective, even if they decided to sell them all in one go, it wouldn’t be the end of the world. At the current total lending to the US government via the Treasury market of more than 14 trillion dollars, China’s holdings represent significantly less than 10% of it. It would cause volatility but be digestible and not crash the market.

Thirdly, it certainly makes sense to watch the total amount of foreign holdings to spot any potential red flags. From September the number fell by 25 billion to 6.2 trillion in October, ie by a mere 0.4%. In other words, the Treasury market remains safe, and no amount of individual jurisdiction’s change in holdings will endanger that. These fluctuations in monthly numbers are perfectly normal, and the patient is getting a clean bill of health.

By the way, Japan as the second largest foreign holder also reduced their stock by 10 billion, and nobody has made a mention of it. At the same time, the order of the ranking hasn’t changed much either. Brazil is still in third place holding in excess of 300 billion. Ireland is fourth with 287 billion, which makes us rest assured that US multinationals still rather park their excess cash offshore rather than incurring a tax bill by repatriating it to America.

The UK is in fifth place, and similarly to Ireland this is obviously not a reflection of British economic performance and sovereign wealth invested in Treasuries but mostly petrodollars captured in the UK clearing system. The disproportionate amounts of 208 billion for the Cayman Islands, as well as 170 billion for Belgium, fall into a similar category. Else, there are no real surprises in the numbers except that Russia features no longer after Moscow disposed of all their Treasury holdings earlier in the year.

Fourthly, to provide one more piece of perspective to the debate, the Fed itself accounts for a far bigger reduction of Treasury holdings than any of the foreign holders, or all of them together. Across the past 2 months, its balance fell by 230 billion dollars, from the all-time high of 2.47 to 2.24 trillion in early December. We will obviously have to see whether this balance sheet reduction will continue at such a pace, as the Fed has been signalling to take the foot off the tightening gas pedal.

But finally, even if the Fed stayed the course of selling stock, even if foreigners were to reduce on a net basis, even if new issues of Treasury bills and notes surged amid the administration producing annual deficits of a trillion for the coming 3 years, I believe the recent strength of Treasury bonds and the material pullback in yields are testaments of the depth of the market and the always underestimated power of domestic investors.

In short, move on, people, nothing to see here…!